in Xing Communication suffered a ban, and the opportunity of China's auto chip company came. Recently, the US Department of Commerce announced that it will ban US companies from selling any electronic technology or communication originals to China ZTE in the next seven years. For ZTE, the devastating blow is not only its traditional business, but also its intelligent networked car business, such as automotive chips and operating systems.

ZTE’s “core†and China’s “chip weakness†were once again exposed.

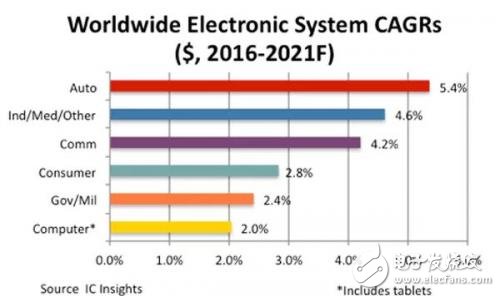

Focusing on the development of the automotive chip business, in recent years, when the performance of the PC semiconductor market has declined year by year, automotive semiconductors have maintained a sustained high growth momentum. According to market research firm IC Insights, by 2021, automotive semiconductors will become the strongest terminal market in the chip industry, and the CAGR of sales of automotive electronic system products will achieve a 5.4% increase.

â–² Global electronic system annual compound growth rate

The reason is that the demand for the number of electronic systems inside the car is constantly rising. More and more car companies, suppliers and technology companies have turned their attention to the realization of auto-driving, V2V/V2I and other car networking functions, while national automakers are gradually increasing R&D investment in electric vehicle technology. Because semiconductors are key components driving the vast majority of automotive innovations, including vision-based enhanced graphics processing units (GPUs), application processors, sensors, and DRAM and NAND flash. As the complexity of automobiles increases, the demand for automotive semiconductor components is bound to grow steadily. Therefore, the automotive sector is a new engine for the semiconductor industry to promote its long-term development.

Although the car accounts for only about 10% of the entire chip industry compared to other sectors, Gartner Group predicts that by 2020, the profit growth rate of the automotive semiconductor business segment will be global chips. Double the market.

Then, at the time of the ZTE incident, it is appropriate to talk about the rapidly emerging automotive chip market and the opportunities for differentiation of Chinese auto chip companies in the development of their own brand “new fourâ€.

Evolving car marketTo be honest, the automotive industry has never experienced so many simultaneous changes. In the past few years, we have witnessed the integration of a large number of new technologies into mass-production models, including matrix LED headlights, lidar sensors and continuously optimized camera sensors. Of course, technologies such as 3D map applications, electric vehicle batteries, and augmented reality have all improved, and 5G communication networks and next-generation travel solutions may soon become a reality. In addition, consumers' preferences and attitudes toward cars are also changing. For example, the number of customers who have the idea of ​​“buying a car is important†continues to decline.

A report issued by consulting firm McKinsey pointed out that by 2030, the global automotive industry will mainly change in the following four directions:

Car electrification

In the next 10 years, as battery prices continue to decline while the number of charging infrastructure increases, by 2020, the number of electric vehicles will account for 5% to 10% of new car sales. Taking into account changes in the level of technological progress, the form of government regulation, and the rise and fall of electricity prices, the proportion of new electric car sales will fluctuate between 35% and 50% by 2030.

2. Increased vehicle connectivity

Whether a car has interconnected functions is strongly affecting consumers' choice of car purchases, and may have a greater impact on their decisions in the future. In 2016, McKinsey found that 41% of respondents reported turning to other new car brands for better connectivity. At the same time, consumers in each country have different levels of awareness of this matter, and 62% of Chinese consumers believe that connectivity will be a decisive factor in their car purchase. In contrast, US and German consumers holding the same view accounted for 37% and 25%, respectively. Correspondingly, the interconnection sector will bring huge profits to car companies. By 2020, it is expected to soar from the current 30 billion US dollars to more than 60 billion US dollars.

3. Self-driving cars gradually land

Although car companies are gradually introducing more ADAS functions into production cars, high-automatic vehicles that can reach Level 4 are expected to be on the road as early as 2020-2025. After that, the number of mass-produced unmanned vehicles will show steady growth. In 2030, 35% of Level 3 autopilots are expected to be on the road, and 15% will be Level 4. However, the effect of commercialization of autonomous driving can be achieved. The factors that restrict it include the evolution of core technology, price, consumer acceptance, and the ability of OEM/parts suppliers to assess and respond to possible security risks.

4. Shared travel service

Although the per capita car ownership rate in developed countries is increasing year by year, with the rapid travel of shared travel and car sharing and network car service, the car ownership rate will slow down or stagnate in the future. Take the North American market as an example. The number of consumers joining the car sharing service has increased by 400% between 2018 and 2015, and this number is expected to reach a new high in the future. According to McKinsey analysts, by 2030, online car or travel sharing services will account for 10% of new car purchases. This trend has also prompted many car companies to share in the travel sector, so as not to lag behind other competitors.

â–² With the readiness of consumers, technology and government, these four major trends will dominate the global automotive industry in the future.

The changes in the four global automotive industries mentioned above will have a major impact on the differentiation and growth of the entire industry. At the same time, the growing income from travel and enhanced connectivity services is probably the most dramatic change. But the impact of these four major trends is not single, they will also promote the development of other areas.

For example, the price of autonomous vehicles (L3/L4) is very high, which will lead to a rise in the profit of new car sales. In the aftermarket segment, the introduction of new travel services will help increase the profitability of this business segment, as shared cars face higher maintenance costs. However, the aftermarket is also facing the risk and pressure of falling profits, because the powertrain system of electric vehicles is cheaper than the repair of fuel vehicles. Even a self-driving car with a collision accident may be better than the same ordinary fuel vehicle. The cost is as low as 90%.

Of course, whether it is ups and downs, the wave of “four transformations†that the auto industry is experiencing will have an impact on the demand for semiconductors and other parts companies.

The value of the automotive semiconductor market in the past and the future

Despite the possible uncertainties, Che Yun believes that with the increasing demand for safety, comfort and connectivity in the automotive industry, the automotive semiconductor market will continue to grow in the medium and long term. In particular, the rapid development of autonomous driving technology will aggravate this trend. In the long run, electric vehicle-related products will also see significant growth, because hybrid models contain $900 worth of semiconductors, while ordinary pure electric vehicles carry more than $1,000 worth of chips, which is far more than the average of 330 in traditional internal combustion engines. The use of US dollar semiconductor products is much higher.

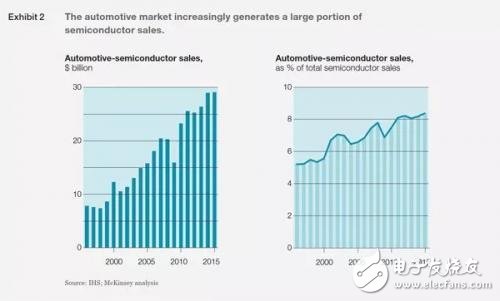

During the two decades from 1995 to 2015, semiconductor products sold to automakers increased from the initial $7 billion to $30 billion. Because of this high growth rate, sales of automotive semiconductor products account for about 9% of the total sales of the entire semiconductor industry. Judging from the current growth trend, sales of automotive semiconductor products will continue to rise during the period from 2015 to 2020, resulting in a 6% increase. The entire semiconductor industry is expected to increase sales by only 3% to 4% during the five years. Therefore, the annual sales of automotive semiconductors may achieve a breakthrough in the range of 39 billion to 42 billion US dollars.

Although there are many opportunities for automotive semiconductor manufacturers in the future, Che Yun believes that different companies have different developments due to different regions, automotive applications and different equipment divisions.

What is a fiber optic slip ring?

A fiber optic slip ring is a device that allows for the transfer of data, power, and signals between two rotating objects. The ring is made up of one or more optical fibers that are used to transmit light signals. These signals can be used to send power, data, or other signals between the two objects. The fiber optic slip ring is a newer technology that has many benefits over traditional slip rings.

How do fiber optic slip rings work?

A fiber optic slip ring is a device that allows electric current and optical signals to pass through a rotating joint. This is often used in applications where it is necessary to transfer data or power between two stationary points while the object rotates. The fiber optic slip ring uses light rather than metal to conduct these signals, which makes it ideal for use in high-speed or hazardous environments.

Types of fiber optic slip rings

When it comes to telecommunications, fiber optics are king. They're the backbone of almost every network today, and they're getting faster and more reliable all the time. That's thanks in part to a technology called fiber optic slip rings.

Advantages of fiber optic slip rings

A fiber optic slip ring is a device used in optical communication. It is a component of many fiber optic networks and it allows for the transmission of data over long distances without losing signal quality. Fiber optic slip rings are also used to improve the performance of other optical systems.

Disadvantages of fiber optic slip rings

Fiber optic slip rings are growing in popularity for rotating applications. Fiber optic slip rings provide many advantages over traditional electrical slip rings, including much smaller size, weight, and power consumption. However, fiber optic slip rings also have a few disadvantages. One disadvantage is that they can be more expensive than traditional electrical slip rings. Additionally, fiber optic cables are more fragile than electrical cables, so they can be more susceptible to damage.

Conclusion: What are the benefits and drawbacks of fiber optic slip rings?

When it comes to fiber optic slip rings, there are both benefits and drawbacks to consider. On the one hand, fiber optic slip rings offer a number of advantages over traditional metal contact slip rings. They are lighter in weight, which makes them easier to install and transport. They also generate less heat, making them safer to use in hazardous environments. Additionally, they provide superior performance in terms of electrical noise and signal integrity.

However, fiber optic slip rings also have some drawbacks. They are more expensive than traditional metal contact slip rings, and they can be more difficult to repair if they malfunction. Additionally, they may not be suitable for some applications due to their limited range of motion.

Fiber Optic Slip Ring,Brass Slip Ring,Fiber Optic Silp Ring,Electrical Rotary Joint

Dongguan Oubaibo Technology Co., Ltd. , https://www.sliprob.com